Insurance Claim Success Story

Allstate Claim – Denial to Approval Through Appraisal

The Situation

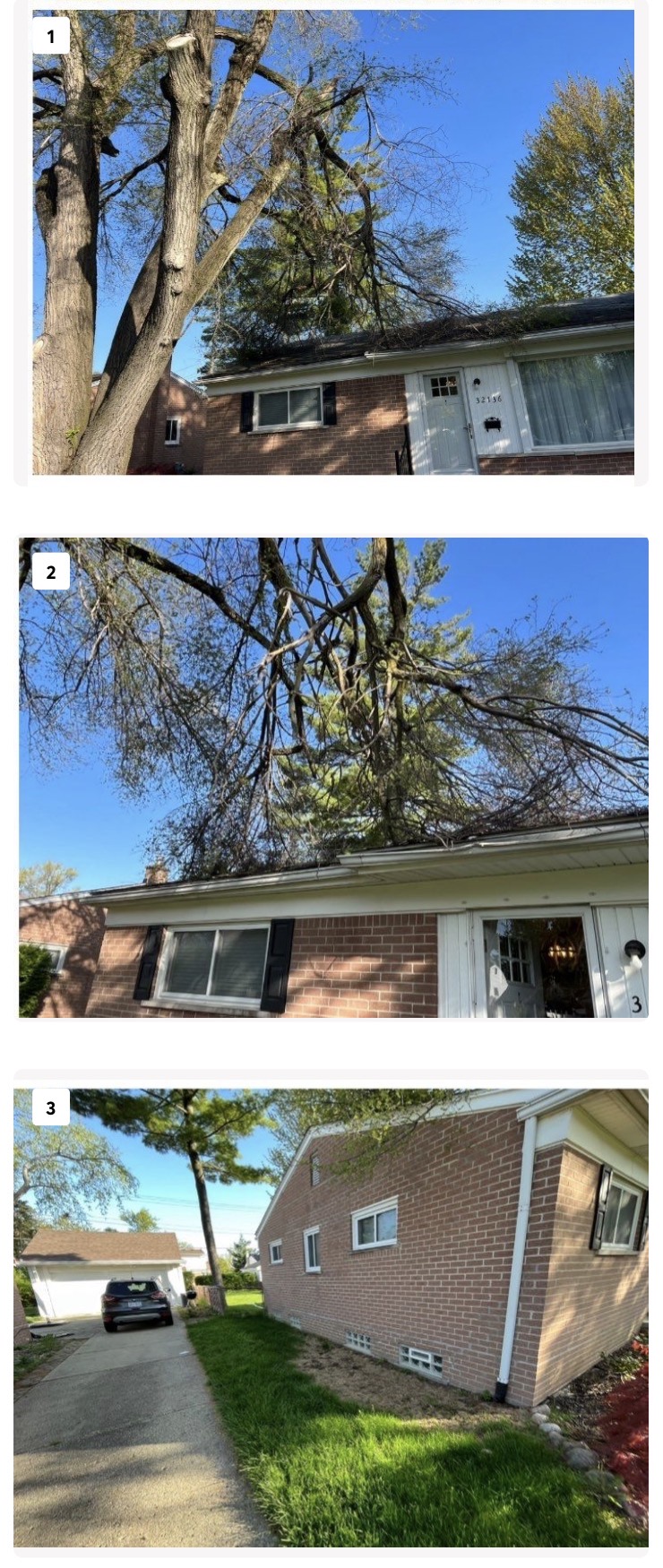

Following a severe ice storm, a homeowner experienced significant property damage when a tree limb fell onto their home. The impact caused:

Structural damage to the roof

Compromised roof decking

Interior damage from water intrusion

Despite the clear cause of loss, the insurance company initially denied the claim entirely.

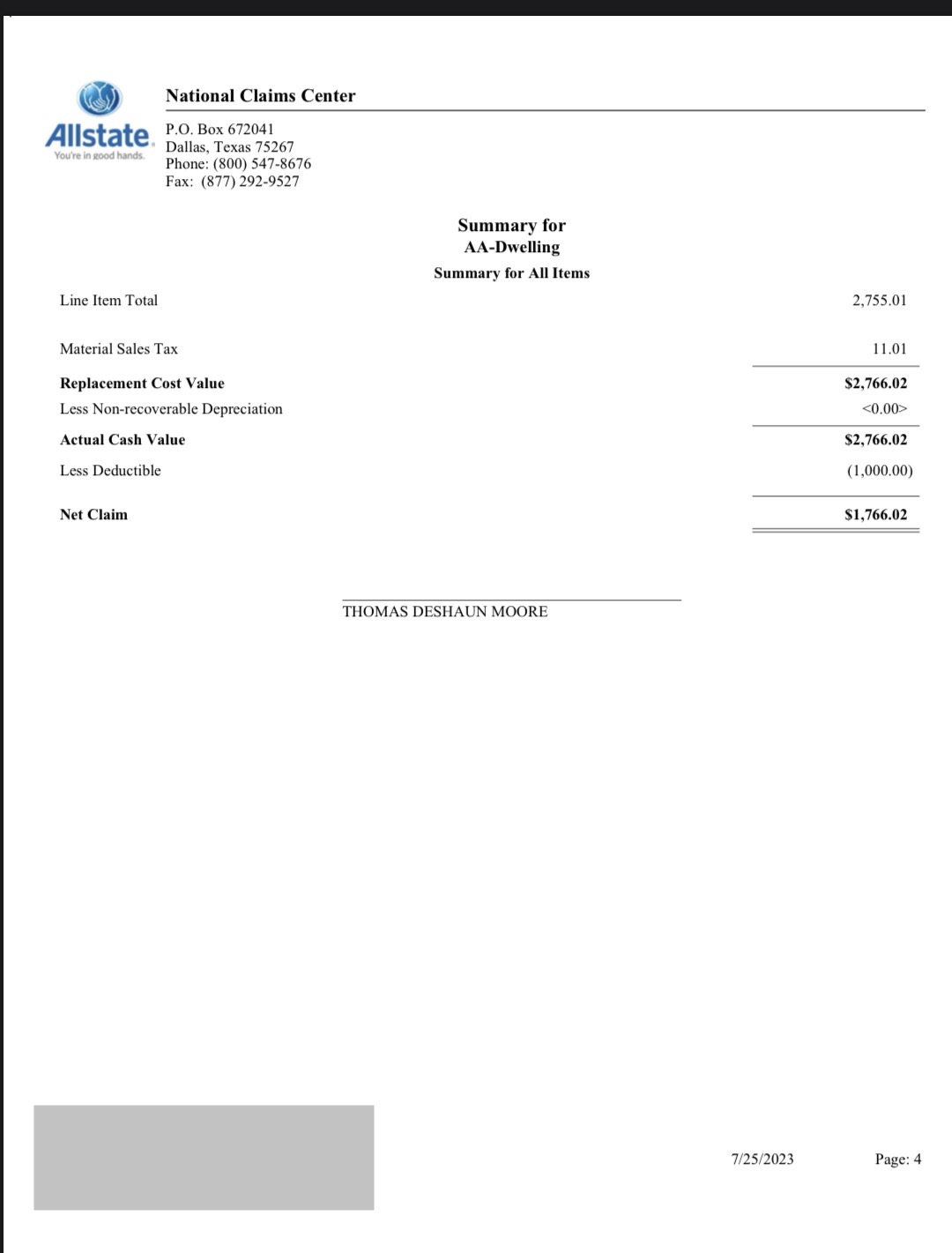

Initial Insurance Decision

After further communication and a reinspection, the insurance company revised their position:

$2,766.02 approved after reinspection

Later increased to $5,027.67

However, both approvals still failed to account for the true scope of damage, leaving the homeowner significantly underpaid.

Protecht Exteriors Investigation

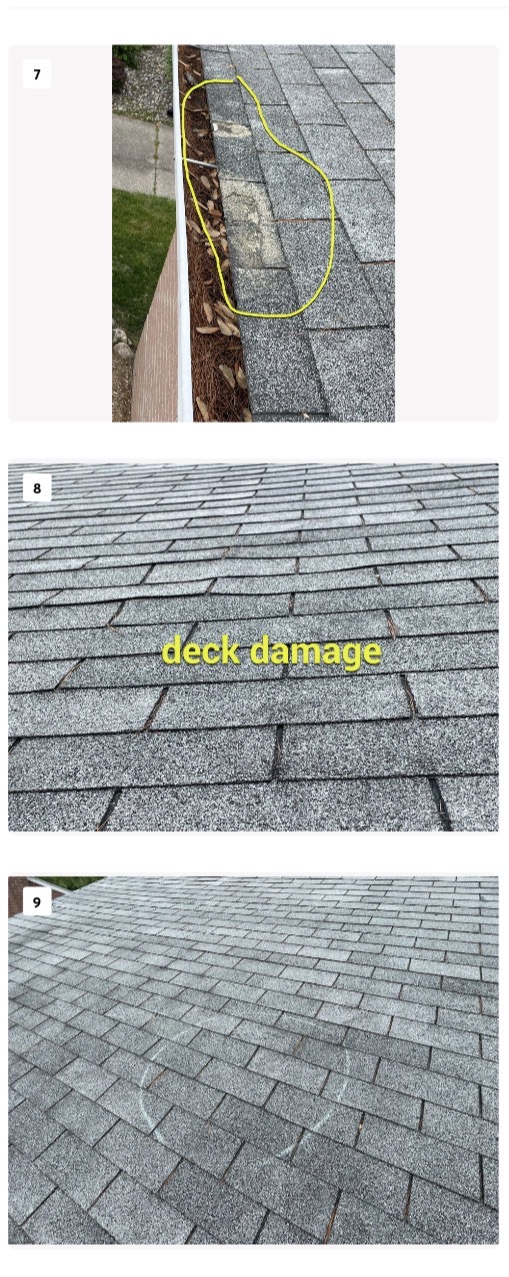

Full photo Damage Report

We Built an in depth damage report to explain the damages

Documented all roof elevations

Showed damage to the decking

Missing shingles

Interior damages

Tree impact points

Engineer Report

We coordinated with an independent engineering firm.

To asses the damage caused by the tree:

✅ Storm-related damage to the home

✅ Structural impact from Tree

✅ Structural intergrity of the home

The home passed all the structural integrity testing and was deemed safe.

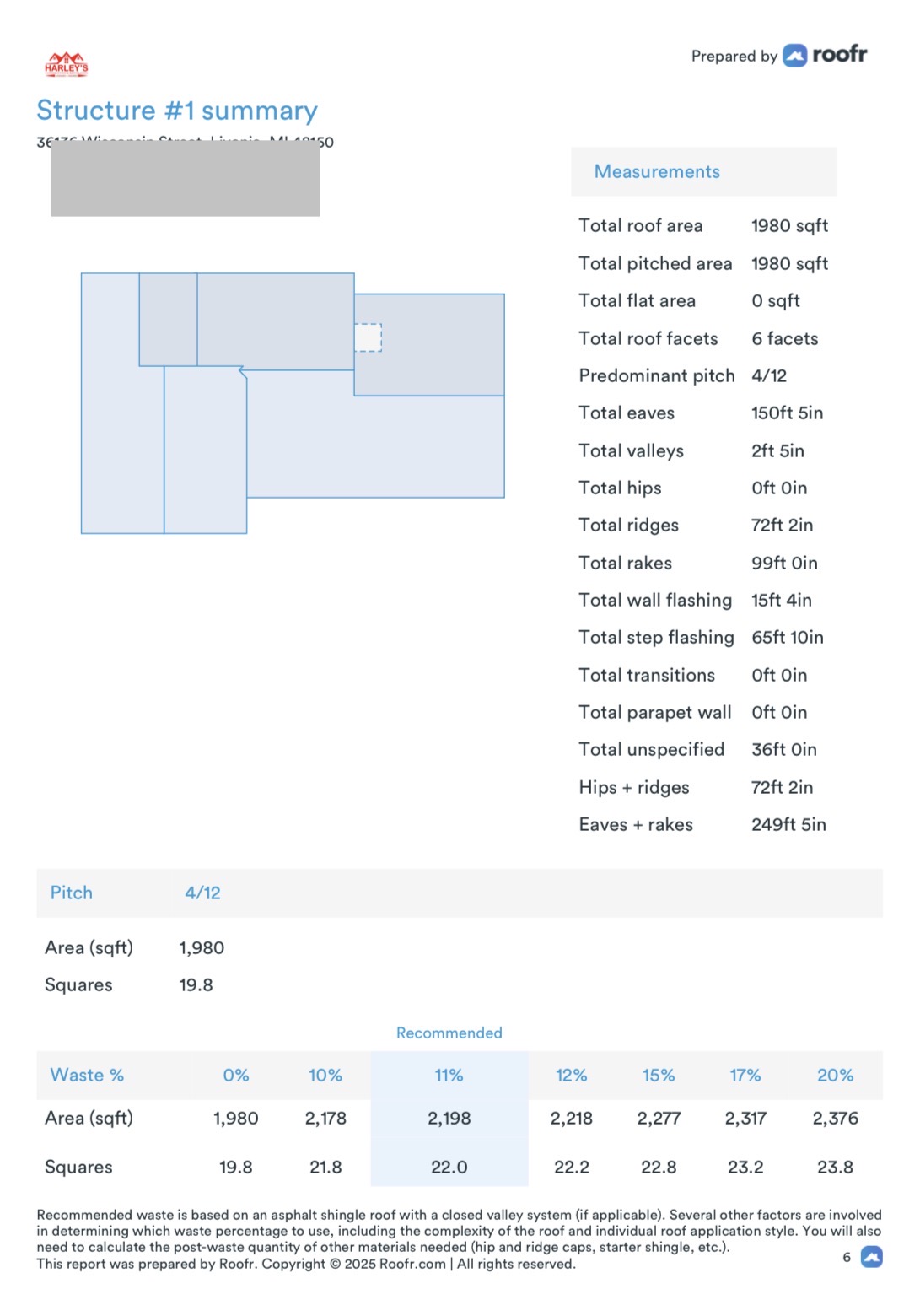

Satellite Measurements

Professional satellite measurements were ordered to determine exact square footage and linear footage for the roof , so the estimate information we provided to the insurance company was 100% correct.

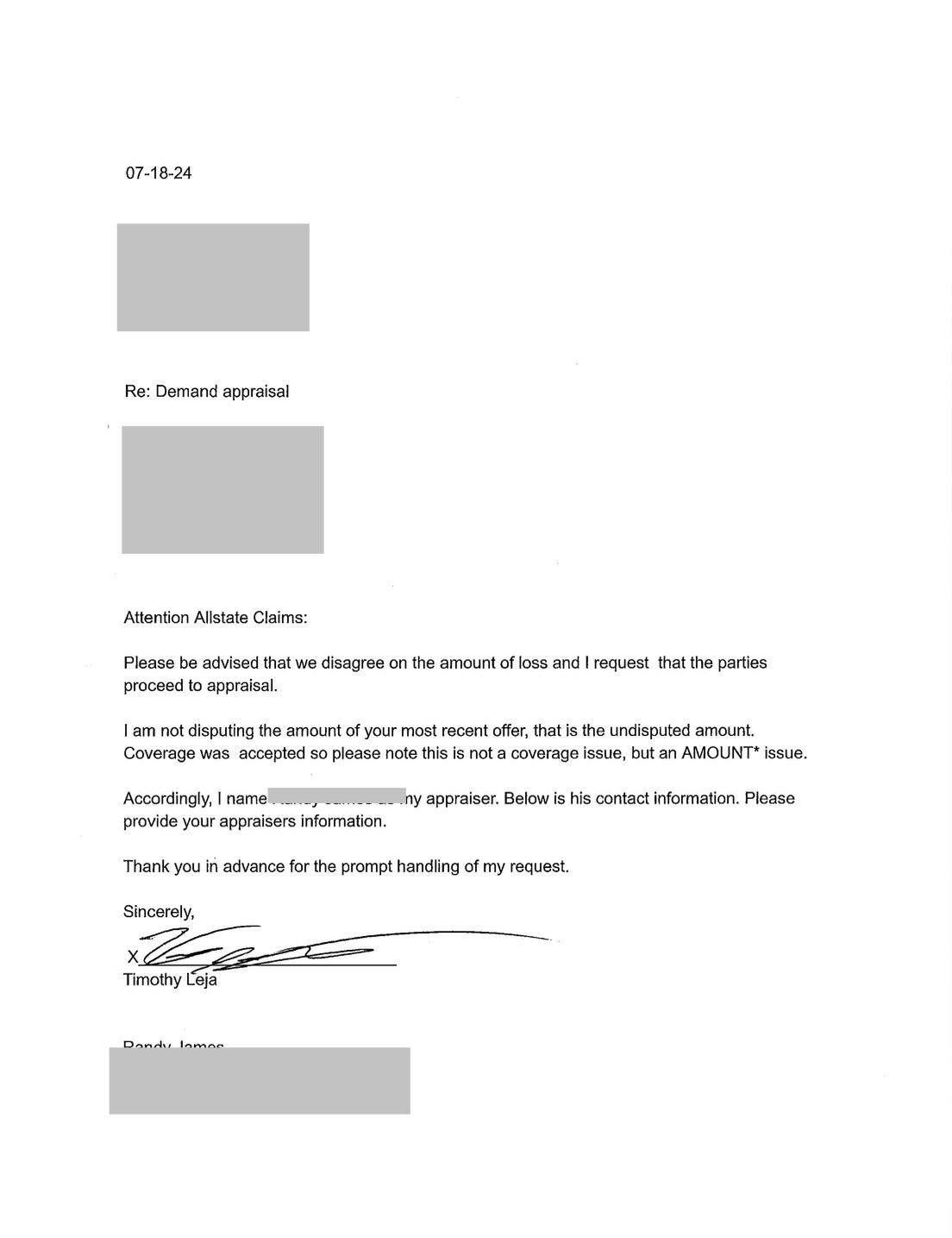

Appraisal Process

The homeowner exercised their contractual right to appraisal.

A licensed appraiser represented the homeowner

The insurance company assigned their own appraiser

Both parties evaluated the full scope of damage

They come to an agreement on the scope of damages

The proper price to restore the property

If the appraiser cant agree an umpire is assigned

two signatures make the appraisal valid

Evidence Submitted To Insurance

A Photo report showing additional Damaged Shingles on Multiple Slopes

Damages documented to decking and interior

Engineer Report for Roofs Structural Intergrity

Satellite Measurements for Roof and Siding

Claim was taken to Appraisal to ensure Proper Coverages

What happened after we submitted the information ?

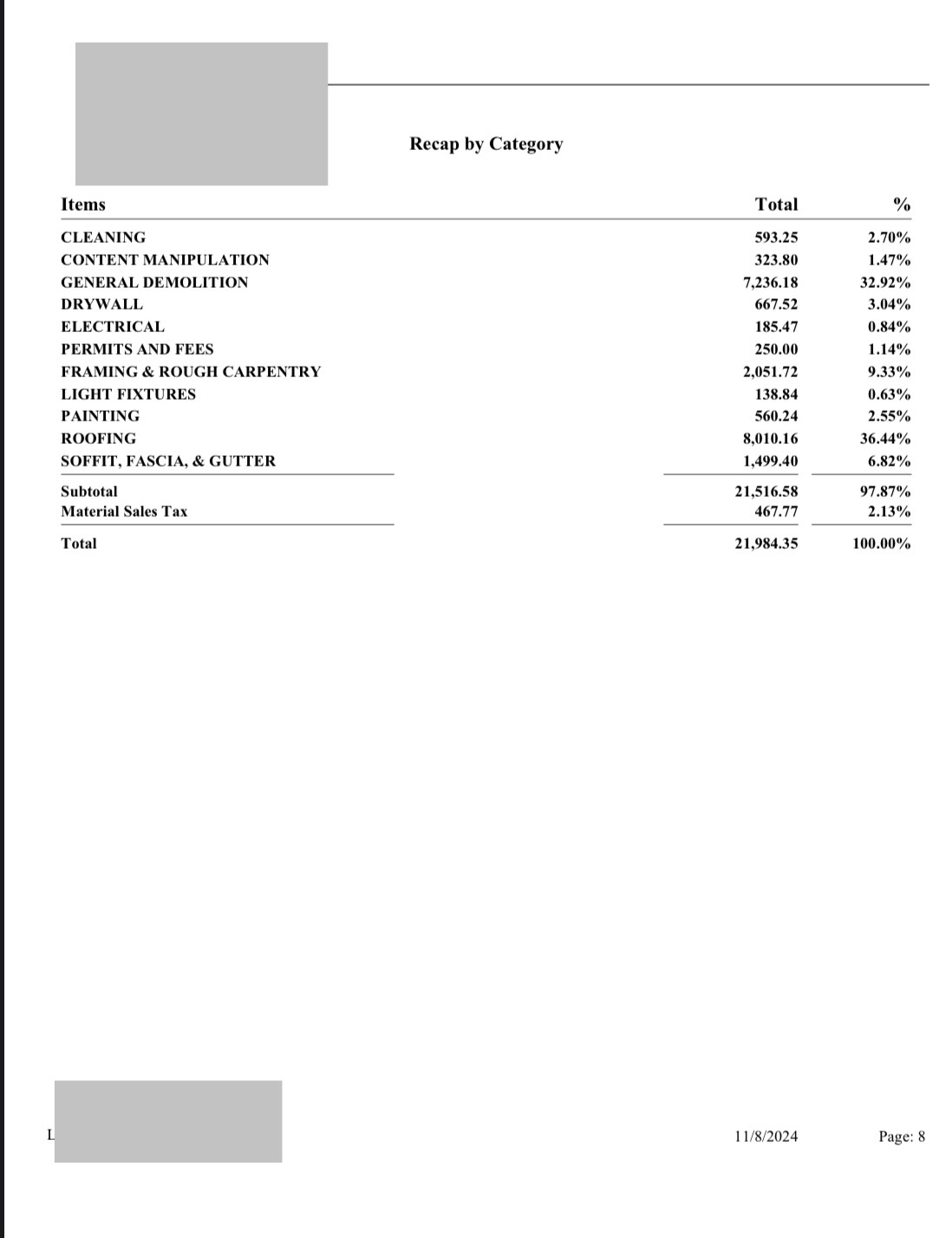

Final Outcome

After the appraisal process and engineering validation:

✅ Final Settlement: $21,984.35

Full roof damage accounted for

Interior damages included

Structural concerns properly addressed

Why This Matters for Homeowners

If your claim is:

Denied

Underpaid

Or only partially approved

There are still options.

With the right approach, documentation, and representation, outcomes can change dramatically.

The Protecht Difference

Identifying overlooked damage

Building evidence-backed claims

Navigating complex insurance processes

Maximizing claim outcomes for homeowners

👉 With the right process, claims can go from DENIAL to full Replacement

Think Your Roof Claim Was Unfairly Denied ?

Schedule a professional inspection with Protecht Exteriors.

Where Technology and Construction meet

Quick Links

Home

Services